The rise of the “Now Economy” has led to an increase in consumer expectations for quick and effortless transactions. If you’re a financial adviser, you sit at the cross section of a colossal data exchange between multiple parties, which puts you in a prime position to respond to these changing expectations. The key is to understand how to use this data and choose the right partners, so you can adapt your business to give your clients what they want and expect.

So what should you focus on first? Here are some strategies that your firm can use to succeed in this environment:

- Communicate relevantly: With all the marketing and spam flooding our inboxes and text messages, it’s important to send targeted, relevant messages that your clients will read and act on. Using data to send timely, relevant communications about mortgage applications, insurance renewals, and other financial products can increase conversions. For example, you can use data to send automated personalized emails reminding clients when their insurance policy is due for renewal or when their fixed rate is coming to an end.

- Use an omni-channel approach: Different generations and demographics have different preferences for communication channels, so it’s important to reach customers through a variety of platforms. SMS and WhatsApp are becoming increasingly popular for quick updates and have higher open and click-through rates than other forms of communication.

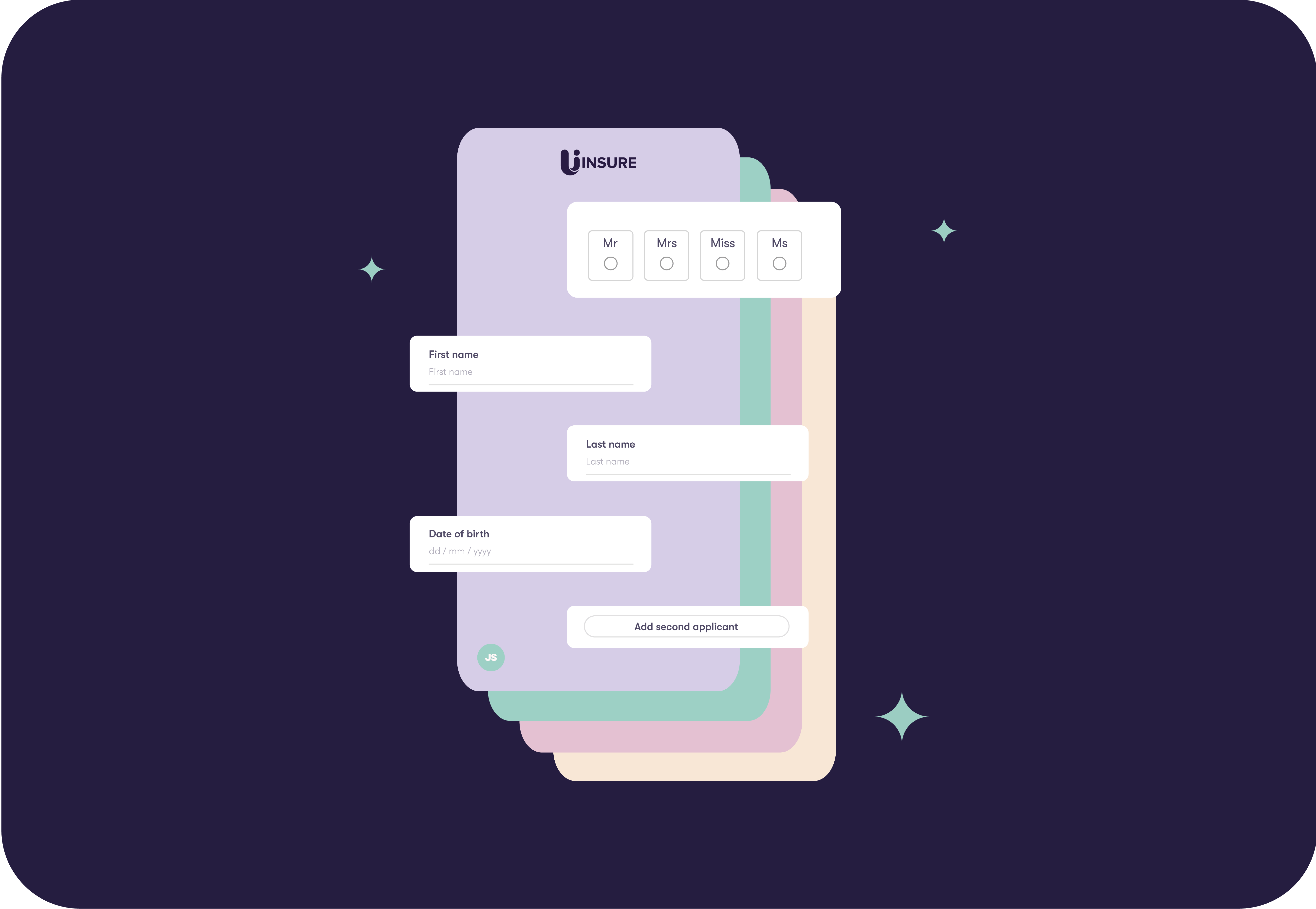

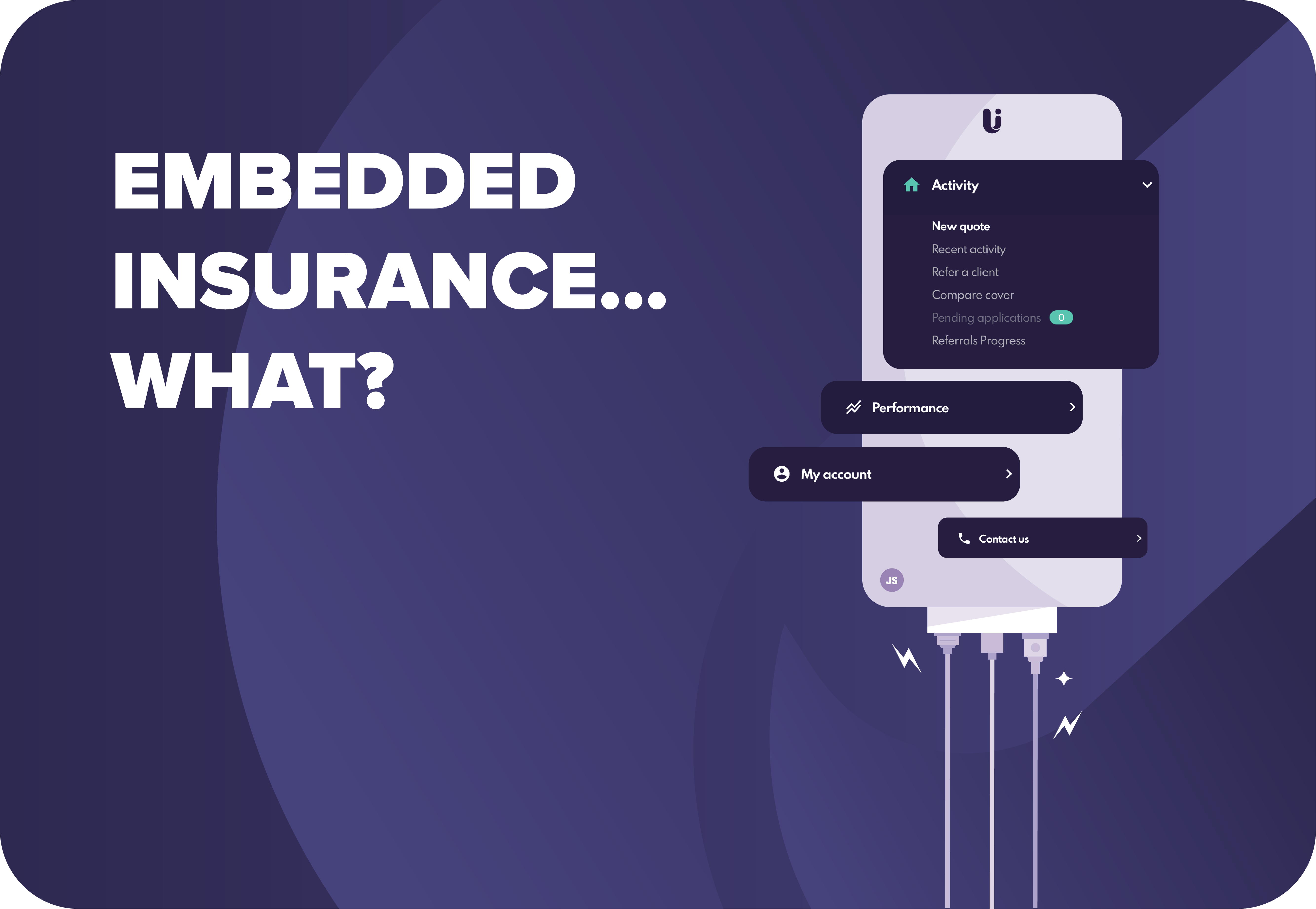

- Utilise technology to streamline processes: Automating tedious tasks can help financial services businesses provide a more efficient and seamless customer experience. By using data and choosing the right partners, businesses can make purchases such as home insurance effortless for consumers.

- Offer flexible payment options: In the “Now Economy”, consumers expect to pay for goods and services using a variety of payment methods. Offer options such as credit and debit cards, mobile payments, and online payment platforms to make it convenient for your clients to do business with you.

- Foster trust and transparency: Trust is more important than ever. Make sure to be transparent about your fees and policies and build trust with your clients by providing excellent customer service and being responsive to their needs (which can also be automated).

The biggest bit of advice? Lean on your suppliers and choose partners to do the hard yards. Give them your problems or needs and let them guide you with their expertise. They should be able to help you identify and implement the right technology solutions.

Share this

Recent Posts

New online commercial and landlord journeys

Uinsure Specialist enjoys successful launch

Smartr365 expands its offering